Project management is a disciplined and process-driven procedure that is relevant to large and small projects. To achieve the desired objectives, planning, organising, and continued monitoring throughout the process are paramount.

Project management in real estate requires the application of skills, tools, and techniques. Furthermore, the complex balancing of competing demands within the process, such as specification, time, and cost.

From refurbishing one room to a whole property or building out a new building completely, these projects are carried out with the purpose of adding value to property generating profit. The knowledge areas in this overview are key to organising, running and completing successful profitable projects. Some of these areas may be done subconsciously or on the back of a piece of paper. The following shows the eight phases of project management and defines their importance in each project.

- Scope management

- Time management

- Cost management

- Quality management

- Communications management

- Risk management

- Procurement/contract management

- Stakeholder management

Key PHASES OF PROJECT MANAGEMENT

Of the eight main elements, there are four essential phases of any project management exercise carried out for real estate.

Scope Management

Usually this is during the conceptual planning stage of a project. The scope of the project should outline the activities, the resources, the personnel, and the specifications in order to create an end product that achieves the objectives of the project.

Time Management

Time is money, as Benjamin Franklin once said. It is a key variable in all projects and has a significant cause-and-effect on all other variables and budgets involved in the project. The management of time is handled by separating it into the following functions:

- Planning: deciding what has to be done, how it will be done, and what will be used.

- Estimating: determining the duration of each activity and its contingencies.

- Programming: establishing the critical path to determining the best time to do each activity in the most logical and effective way to minimise the project time and ensure all stages are resourced correctly.

- Control: ensuring that the planned or expected time stages are maintained.

Cost Management

This is the key differentiator between a successful project and a flop. There are different stages in cost management depending on the type of project. Regular contractor meetings throughout the project are key to ensuring both parties expectations are in line when modifications occur.

Cost Planning: establishing budgets, standards, and a monitoring system. This could be estimations put into initial budgets to run financial feasibilities before purchasing a property or initial plans to repurpose and currently owned property.

Cost Estimation and Forecasting: assembling, analysing, and predicting multiple general contractor quotes. Furthermore, using them to set financial forecasts for the project.

Cost Control: gathering, accumulating, analysing, monitoring, reporting, and managing the cost on an ongoing basis throughout the duration of the project.

Cost summary: value analysis and other specialist views of cost to summarise the project’s conclusion.

Quality Management

This involves ensuring requirements and specifications are maintained through quality assurance and quality control.

This involves the general management of contractors, professionals, and other stakeholders involved in the project. Furthermore, it starts from the first time the project is discussed to the final inspection to confirm that the work has been done to the desired satisfactory standard.

THE OTHER 4 KEY PHASES INVOLVED IN PROJECT MANAGEMENT

Risk Management

This is the process of understanding, identifying, and assessing risks that might be apparent in the project. For example, this includes, but is not limited to, financial, health and safety, or reputational risks. The two stages involved in risk management are:

Risk identification: determining what are, or are likely to be, the critical uncertainties that will likely arise in the project.

Risk response: deciding how to proceed with the highlighted risks. The options available are to avoid entirely, reduce exposure, transfer to someone else, or retain the risk.

There is also an acknowledgement and allowance for risks that are not obvious from the outset and would be unforeseen during the project. A contingency allowance within the budget and timeline provides cover for these types of unforeseen risks.

Procurement/contract Management

The procurement process establishes a competitive tender in order to gain competitive pricing and other specific details for the project. Furthermore, proof of a track record will all help to compare quotations and award the winning party. The contract between the client and suppliers is the key document in the relationship. The contract represents the objectives and responsibilities of the parties and holds each accountable to complete the project.

Communication Management

Project communications provide the link between people, ideas, information, and feedback throughout the project. This is an essential part of the process, and if done well, it will ensure the project stays on track. Although done poorly, the project has a high chance of delays or even failure.

Stakeholder management

The identification, management, and control of the project stakeholders is a key aspect. Stakeholders can be individuals, groups of individuals, or businesses that have an interest in the project. Typical stakeholders are as follows:

- Client

- Project Manager

- Project Sponsor/investors

- Suppliers

- Contractors

- Buyers

For stakeholders such as investors or clients, maintaining the agreed-upon communication cadence provides peace of mind. This can be in the form of agreed-upon weekly or monthly report structures.

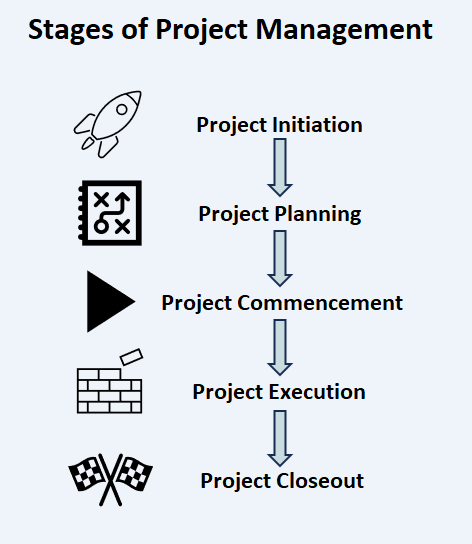

WHAT ARE THE STAGES OF A REAL ESTATE PROJECT

There are multiple stages within the lifecycle of a project, which are listed below. The key functions above are used in different capacities throughout the stages to ensure a successful project is complete. The stages are as follows:

WHAT PROJECT MANAGEMENT ACTIVITIES HAPPEN IN THE PLANNING PHASE

The planning stage should cover the vast majority of functions in order to establish the outcomes of the project.

- Stakeholder mapping, analysis, and selection

- Scope Management: collecting requirements and defining the scope

- Time management entails establishing a schedule, defining activities, sequencing activities, estimating resources, and determining the overall duration.

- Cost management: determining estimates, budgets, and feasibility of the project

- Communication management throughout the different parties involved in the process ensures clarity and accuracy to make sure the planning is as effective as possible.

- Risk management identify risks, analyse them, and plan the responses to incorporate into the project scope.

This is a high-level summary and example of what functions are apparent at a certain stage of a project. For further and in-depth breakdowns of each stage of project management, please read The Fundamental Stages of a Real Estate Project.

For more information and courses, the Project Management Institute has specific real estate construction courses that delve deeper into the subject.